Mortgage Rates | Beware of Refinance Headlines

Bradley Katzen September 3, 2024

Bradley Katzen September 3, 2024

I hope everyone is enjoying the final months of summer!

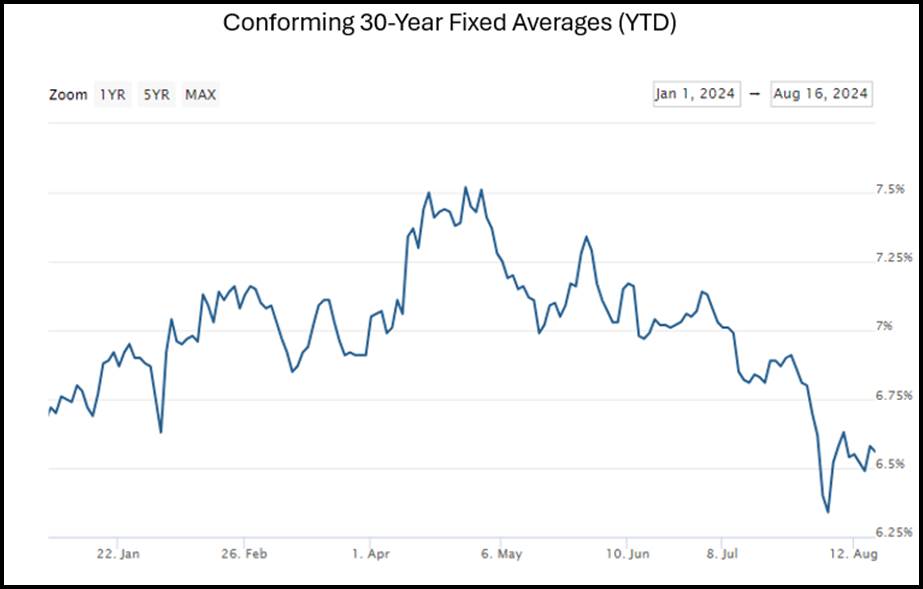

Purchase interest rates are looking pretty, pretty, pretty good. The past couple of weeks have offered opportunities in the upper 5s at an extreme, and low-to-mid 6s at scale for most borrowers & programs. The Conforming 30-Year Fixed average closed yesterday reporting 6.500%.

Today’s topic: refinancing and falling rates as we are inundated by social & media headline grabs. Refinance interest rates are looking pretty, pretty good too, but only for the few.

Primed for Poor Financial Decisions & Misguidance from the Mortgage Industry

I’m not saying its premeditated, but you and your clients should understand that not all mortgage professionals are created equal in their motives, expertise, nor understanding of financial cost-benefit analysis, and therefore their guidance to customers can often be short-sighted, missing key factors, or even just involving their own self-interest (in seeking a commission). A refinance market opportunity is a primed playground for this activity, and millions fall victim without truly understanding the trade-offs and expenses as it relates to any rate improvement. Compounding the financial injustices committed by the industry is the pace at which homes are appreciating, allowing lenders to show refinance options to borrowers with elevated costs ‘rolled into the loan amount’ (financed) where their focus is only directed to the visually attractive lower interest rate and absence of needing to come out of pocket with any cash; deceiving the eyes and mind as if it’s free lunch and no-brainer deal. Sometimes it is, sometimes its more nuanced.

Refi Demand Exploded (Relatively), But Rates Are Settling (For Now)

There's been widespread speculation as to the effect that falling rates will have on refinance demand in a world where 2/3rds of mortgages have fixed rates under 4%. This week's data suggests it's worth discussing; referencing the charts below reading from left to right. While the blue bars in the ‘Share of Loans by Fixed-Rate’ on the right side within the first chart may not be as big, they still represent 100s of millions of dollars of loan balances. In fact, there are nearly 10 billion dollars outstanding at rates of 7% and higher. As such, when last week's rates dropped briefly into the low 6% range (key factor- with paying at least 1% discount points), there was a mini glut of refi demand making BIG HEADLINES. The middle chart shows the latest refinance application index from the Mortgage Bankers Association (MBA) this past week. That may not look too "mini" at first glance, but context is important. In other words, we're barely back to what had been historically low levels of refi activity seen in late 2018 shown in the final chart ‘ Historical Refi Activity’. The counterpoint is that rates were only in the low 6's for an hour or two last Monday morning with very large ‘spreads’ as it relates to discount points, with mortgage investors demanding points which is typical in high-volatility times but offering far-improved rate levels relative to the scope (cost) of the points. As an example, a purchase or refinance applicant may have achieved 6.125% with paying 1% discount points but a zero-point option was closer to 6.875%-7.000% even with the big improvement. In this case, the ‘spread’ is the difference between a zero-discount point interest rate offering vs. the rate achieved by paying points. By the end of this week rate pricing normalized, where paying 1% discount point achieved a rate between 6.500% and 6.625% on average, where the zero-point option was still around 6.875%-7.000%. Bottom line: this is still proof of concept for more widespread refi demand in a scenario where rates move back into the 5s and hold those levels for more than a few hours in a stabilized market environment.

Refinance Math is Complicated unless it’s not performed- then it’s easy.

Lenders, especially ‘refi shops’ where refinances are their core business activity, are notorious for attempting serial-refinancing via marketing bombardment and lazy or completely absent cost-benefit analysis. Refinancing in general comes at a baseline cost of roughly $5,000 with some plus/minus variance depending on geographical location (county/state, city). That number doesn’t account for any discount points paid which would be considered an additional expense, or re-establishment of escrow for property taxes & insurance when applicable which is not considered an additional expense since they exist on the current loan, but still must be accounted for in the new borrowed amount (loan size). Many refinance customers are exchanging a 30-Year Fixed for a new 30-Year Fixed, and therefore restarting their loan’s amortization schedule to be again front-loaded with mostly loan interest being paid (albeit at a lower rate). What happens here is the newly extended term amplifies the appearance of greater savings because it’s spread out over a new 30-years. This is where expected home appreciation trends and forecasted timeline of continued ownership become two more key ingredients into the equation, along with many more which will be summarized in an upcoming memo to follow. Lasty is the anticipated rate trajectory. If one believes we’re in only the early inning of falling rate levels, then multiple refinances and their associated costs with increasing loan sizes to absorb said costs could be a major financial setback in the big-picture, or even catastrophic in the short-term realization, unless properly accounted for in the new loan’s structure & analysis.

Borrower beware of the headline noise and who they seek financial advice from. If you have clients involved or interested in the refi process, encourage them to consult with us for a review of their situation and truthful & transparent opinion. Yup, free professional advice.

I hope this topic and insight was thought-provoking and useful.

8/17/2024 content courtesy of Bradley Katzen

Senior Mortgage Consultant

Production Recognitions

Chairman’s & President’s Club | Elite Team Member | Top 1% in Country

Licensed: DC, MD, VA

Cell: +1(301)-943-9316

July 23, 2026

July 23, 2026

July 23, 2026

July 16, 2026

July 16, 2026

July 16, 2026

July 16, 2026

July 9, 2026

October 3, 2024

New Eligibility & More Changes: Oct 2024

Get assistance in determining current property value, crafting a competitive offer, writing and negotiating a contract, and much more. Contact us today.