Mortgage Credit Certificates, also known as an "MCC", are available to eligible homebuyers through their State Department of Housing & Community Development, and can save homeowners tens-of- thousands of dollars by reducing the amount of federal taxes they owe each year.

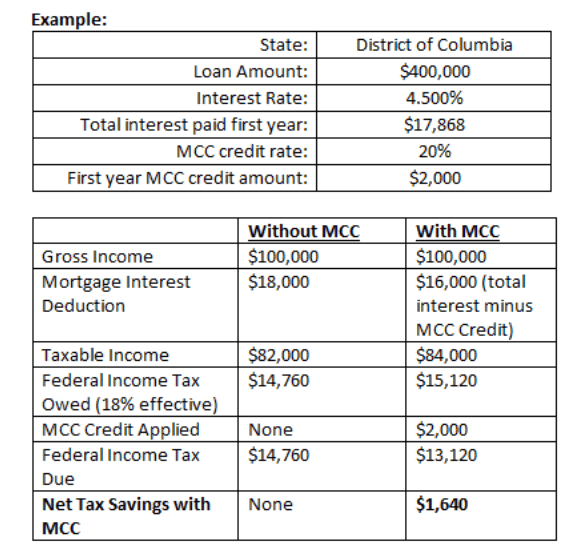

An MCC allows a first-time homeowner to claim a tax credit for some portion of the mortgage interest paid each year for the life of their loan up to $2,000/annually, in addition to claiming the remaining standard allowable mortgage interest tax deduction which reduces taxable income.

A tax credit is not the same as a deduction, as a tax credit is a dollar-for-dollar reduction in the amount of federal tax you owe, therefore reducing your actual tax liability.

MCC's are available to buyers utilizing Conventional, FHA, VA, and USDA financing programs. Each State has slightly differing MCC eligibility guidelines and requirements, such as:

-

Buyers must not have occupied a home they owned in the previous three years.

-

Buyers must meet income & purchase price restrictions.

-

Buyers must intend to use the new home as their primary residence.

However, some restrictions may be waived for properties identified as being in "targeted" areas identified by state & local governments or for veterans, in some cases.

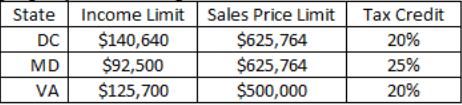

Below are a few highlighted minimum restrictions for a family-size of two or less, though there are some variances by State, with income & purchase price limits increasing with larger family-size or if a property is in a "targeted" area:

The cost of MCC's range from $450 to $1,500, depending on the State of issue and whether the MCC is used as a stand-alone, or in conjunction with assistance programs such as DC Open Doors, HPAP, MMP, or VHDA. However, homeowners typically will recoup any cost within their very first year of receiving the tax credit.

There are other considerations when determining if an MCC will be beneficial for a homebuyer, such as the IRS's recapture of federal mortgage subsidy rule which may have negative costly impacts when selling their home. That said, it's extremely important that the homebuyer be properly educated by a qualified, reputable lender, and their licensed tax advisor.

Not all lenders are eligible or qualified to participate in offering MCCs, which is another thing your buyers should be aware of when seeking guidance.

Prosperity is a participating lender to issue MCCs in the majority of States where we lend, and our team specifically, is well-versed in the subject matter and in a position to provide your buyer with the tools & resources to make an educated decision about their loan options, including the application of a Mortgage Credit Certificate.

Written by: Bradley Katzen